FT Partners Quarterly InsurTech Insights and Annual Almanac

FT Partners is the only data source for comprehensive, global InsurTech deal activity covering M&A, Financing and IPO statistics and trends

FT Partners’ InsurTech Insights Reports are published on a quarterly basis, along with a comprehensive year-end Almanac. All information included in the reports is sourced from FT Partners’ Proprietary Transaction Database, which is compiled by the FT Partners Strategic Insights Team through primary research and data analysis. The reports feature M&A, financing and IPO statistics and trends as well as breakdowns by vertical, geography, investor-type and much more.

View our Global FinTech Insights and Almanac reports here.

Be sure to check back for quarterly updates and additions. All recent reports can be viewed or downloaded for free below.

Report Features:

Q1 2026 and historical InsurTech financing and M&A volume and deal count statistics

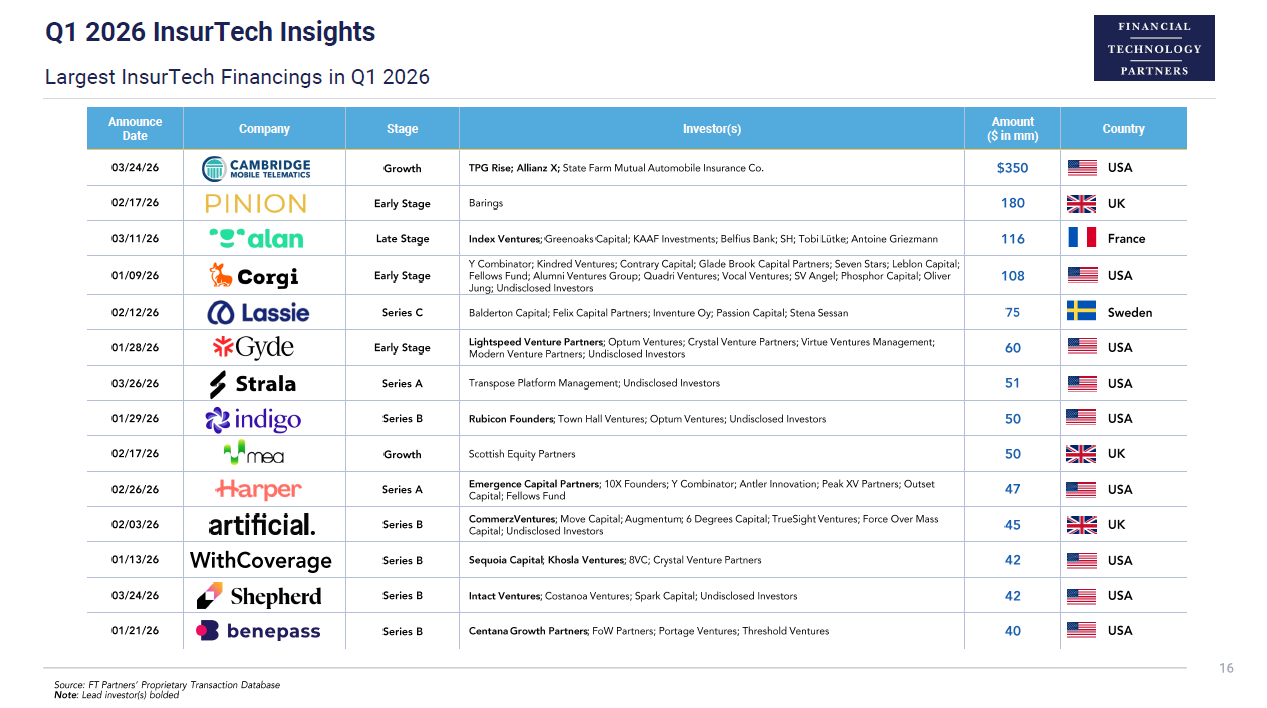

Largest InsurTech financings and M&A transactions in Q1 2026

Most active InsurTech investors

Breakdowns by geography, product type and business model

Corporate VC activity and strategic investor participation

Other industry, capital raising and M&A trends in InsurTech

Key Highlights:

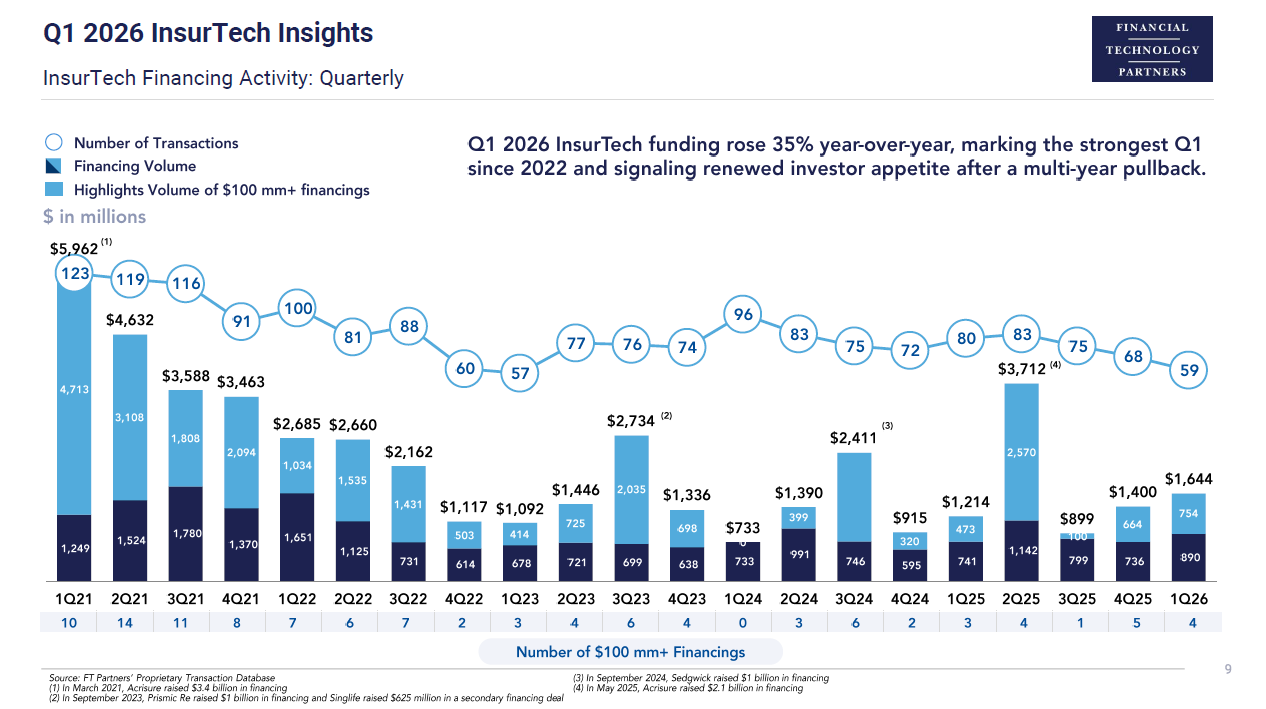

InsurTech financing volume in Q1 2026 totaled more than $1.6 billion, representing a 35% year-over-year increase and a 17% sequential increase over Q4 2025, marking the strongest Q1 since 2022 and signaling renewed investor appetite after a multi-year pullback.

While volume climbed, financing deal count dropped, only by 13% sequentially from the end of 2025, but by 26% from Q1 of last year. This matches the broader FinTech market which experiences falling deal count while volume levels held steady.

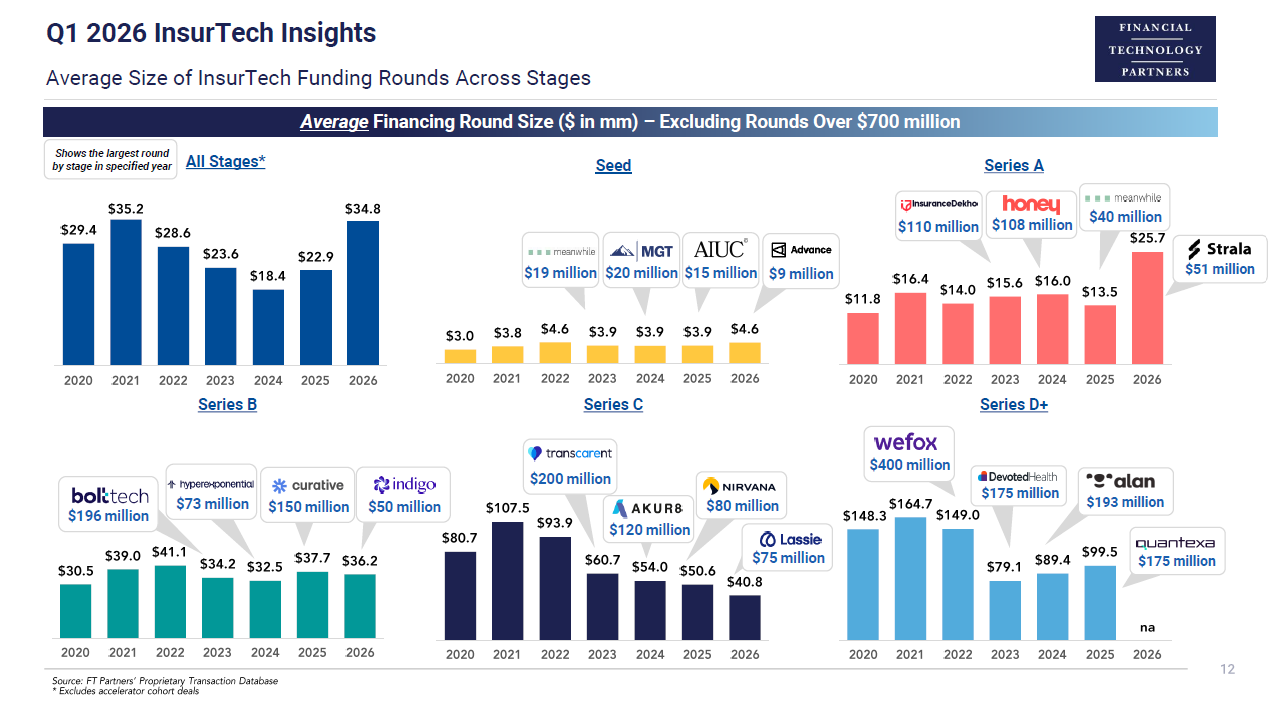

InsurTech Series A rounds reached the highest ever average value at nearly $26 million in Q1 2026, compared with $13.5 million in 2025, boosted by several large deals: AI-powered claims platform Strala’s $51 million round, commercial insurance brokerage Harper’s $47 million combined seed and Series A round, and provider of AI solutions for insurance operations Notch’s $30 million round.

With several M&A deals with undisclosed sale prices in Q1 2026, total M&A dollar volume was quite low. On an annualized basis, deal count is tracking below the record high in 2025, though is in line with other recent years. Notable deals in the quarter included TowerBrook’s acquisition of majority interest in Italy-based insurance claims management services provider MSA Mizar at an enterprise value of more than ~$400 million, Admiral Group’s $109 million strategic acquisition of commercial fleet insurance provider Flock, and Warburg Pincus’ majority investment in lease guarantee provider The Guarantors.

View More Reports